|

Notification of Sale is released in the newspaper of general flow in the county where the property lies (around 3-4 months after nadine b the preliminary procedures are begun by the lender.) Once again it differs from one state to another. Redemption Period. Borrower has statutory redemption period in which to redeem the home, pay all costs and costs and arrearages to bring the home mortgage present.

Foreclosure auction or Sheriff's Sale is held at the court home steps (judicial foreclosure) or other designated place approximately 5 months or more after initial foreclosure proceedings are set up by lender. If the property is not cost the foreclosure auction or Constable's Sale, then it becomes an REO (bank owned realty) home which is now owed by the bank (who took over abn amro mortgages). This typically occurs roughly 6 months to year after foreclosure procedures were begun. House owners do have alternatives to save their home from foreclosure. Doing absolutely nothing is the worst possible thing you can do. Don't panic - what is a non recourse state for mortgages. The most intelligent method to save your house from foreclosure is to begin discovering a service early on. It is likewise extremely suggested that you talk to a foreclosure defense lawyer to learn what your finest choices are to save your home or a housing counselor. Here is a list of the common alternatives that are available to property owners facing foreclosure: Refinancing and Working Out Reverse Home Mortgage Personal Bankruptcy Litigating Offering Up Your House If you have equity in your home, then you may qualify to re-finance your home loan. When you re-finance, the old loan is paid off with the brand-new loan, which is generally at a lower rate of interest. When you get a home mortgage adjustment, the existing loan is modified by either minimizing the rate of interest, adding the balance dues to the back end of the loan or often the lender will forgive some of the debt and/or extend the loan term from 30 years to 40 years. Otherwise it will not reduce your monthly Article source home mortgage payment enough to make a difference. Another option when negotiating with your lender is to request a reinstatement of your loan. This implies that you must pay all the arrearages and any costs to bring the loan present (mortgages what will that house cost). A repayment plan is also an alternative. When the loaning husband passed away in 2016, the loan provider set up a foreclosure action that has resulted in the non-borrowing spouse needing to vacate the property. "Even when both hubby and better half are old adequate to certify, reverse home mortgage lenders often encourage them to eliminate the younger partner from loans and titles," the short article reads. Indicators on There Are Homeless People Who Cant Pay There Mortgages You Need To Know

In 2015, the Federal Real Estate Administration (FHA) launched a series of guidelines that were developed to reinforce protection for non-borrowing spouses in reverse home mortgage deals. In the modified guidelines, lenders were enabled to postpone foreclosure for particular qualified non-borrowing spouses for HECM case numbers appointed before or after August 4, 2014. A lending institution might likewise continue by permitting claim payment following the sale of the home by heirs or the debtor's estate, or by foreclosing in accordance with the terms of the home loan and filing an insurance coverage claim under the FHA insurance agreement as endorsed. "A foreclosure is a failure, no matter the trigger," said one of the post's sources. " There is a distinction between foreclosure and eviction that isn't actually described in the article," stated Dr. Stephanie Moulton, associate teacher of public policy at Ohio State University in an e-mail to RMD. "We would require to know the proportion of foreclosed loans that ended due to the fact that of death of the customer, versus other reasons for being called due and payable (consisting of tax and insurance coverage default)." Among the factual issues underlying a few of the concepts of the short article is that it provides older problems of the HECM program in a modern-day context, without addressing a number of the most relevant modifications that have been made to the program in the years given that a lot of the profiled loans were stemmed, particularly throughout an unstable duration for the American housing market: the Great Economic downturn. " The other thing to bear in mind about this particular time period is the collapse of home values underlying HECMs that worsened crossover riskwhich would increase the rate of both kinds of foreclosures," Moulton stated. "And, this was prior to numerous of the changes that have actually been made to secure borrowers and fortify the program, including limits on upfront draws, 2nd appraisal guidelines, and financial assessment of debtors." This includes the aforementioned protections set up for non-borrowing partners, in addition to modifications including the addition of a financial assessment (FA) regulation designed to reduce relentless defaults, specifically those related to tax-and-insurance defaults that frequently afflicted the HECM program in years prior to its execution. The National Reverse Home Loan Lenders Association (NRMLA) is preparing an industry response to the ideas and conclusions provided by U.S.A. Today, according to a declaration made to RMD. "A reverse mortgage is one potential and necessary element for many Americans seeking to fund retirement," said Steve Irwin, executive vice president of NRMLA in a call with RMD. Home Equity Conversion Mortgages for Seniors Reverse mortgages are increasing in popularity with seniors who have equity in their homes and wish to supplement their income. The only reverse home mortgage insured by the U.S. Federal Federal government is called a House Equity Conversion Home Mortgage (HECM), and is just readily available through an FHA-approved lender. The How Is The Average Origination Fees On Long Term Mortgages Diaries

The quantity that will be available for withdrawal differs by customer and depends on: If there is more than one debtor and no qualified non-borrowing partner, the age of the youngest customer is used to determine the quantity you can borrow. You can also utilize a HECM to purchase a main residence if you have the ability to use cash on hand to pay the distinction between the HECM profits and the sales rate plus closing expenses for the residential or commercial property you are acquiring. If you're age 62 or older, you can receive money wesley management from your mortgage company by borrowing against the value of your home through a reverse home mortgage. The payments you get along with accrued interest and other charges increase the loan's balance and decrease your equity in the property. Most reverse home loans are insured by the Federal Housing Administration (FHA), as part of its Home Equity Conversion Home Mortgage (HECM) program. If the property is sold or the last making it through borrower no longer inhabits the home or dies, the loan ends up being due and payable. Generally, the house is sold to repay the loan and, if FHA-insured, FHA pays for quantities not fully covered by the sale profits. Not comprehending your responsibilities under a reverse home mortgage can cause serious effects, consisting of foreclosure.

0 Comments

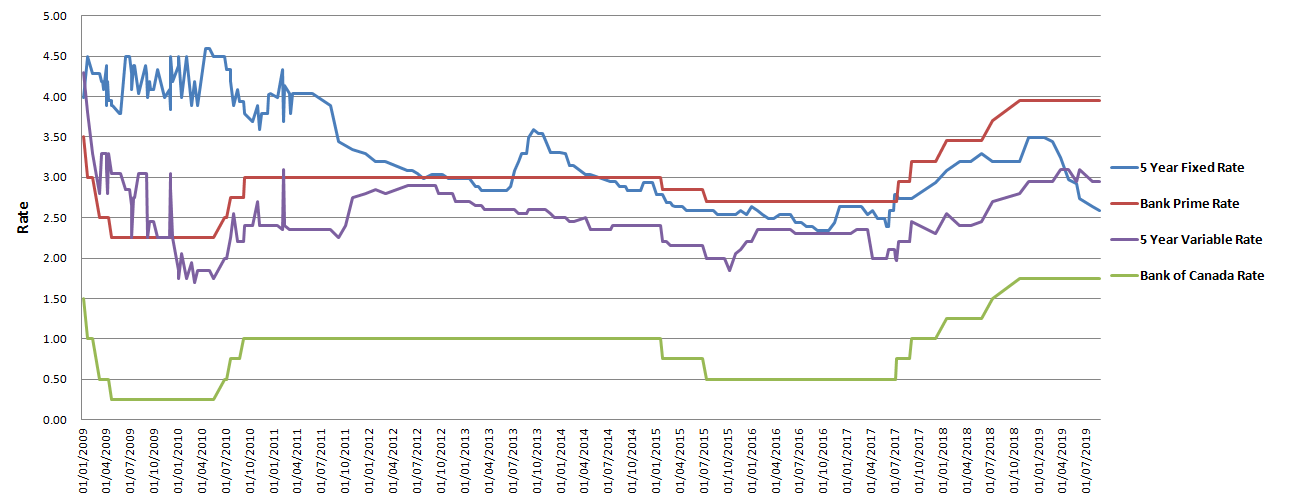

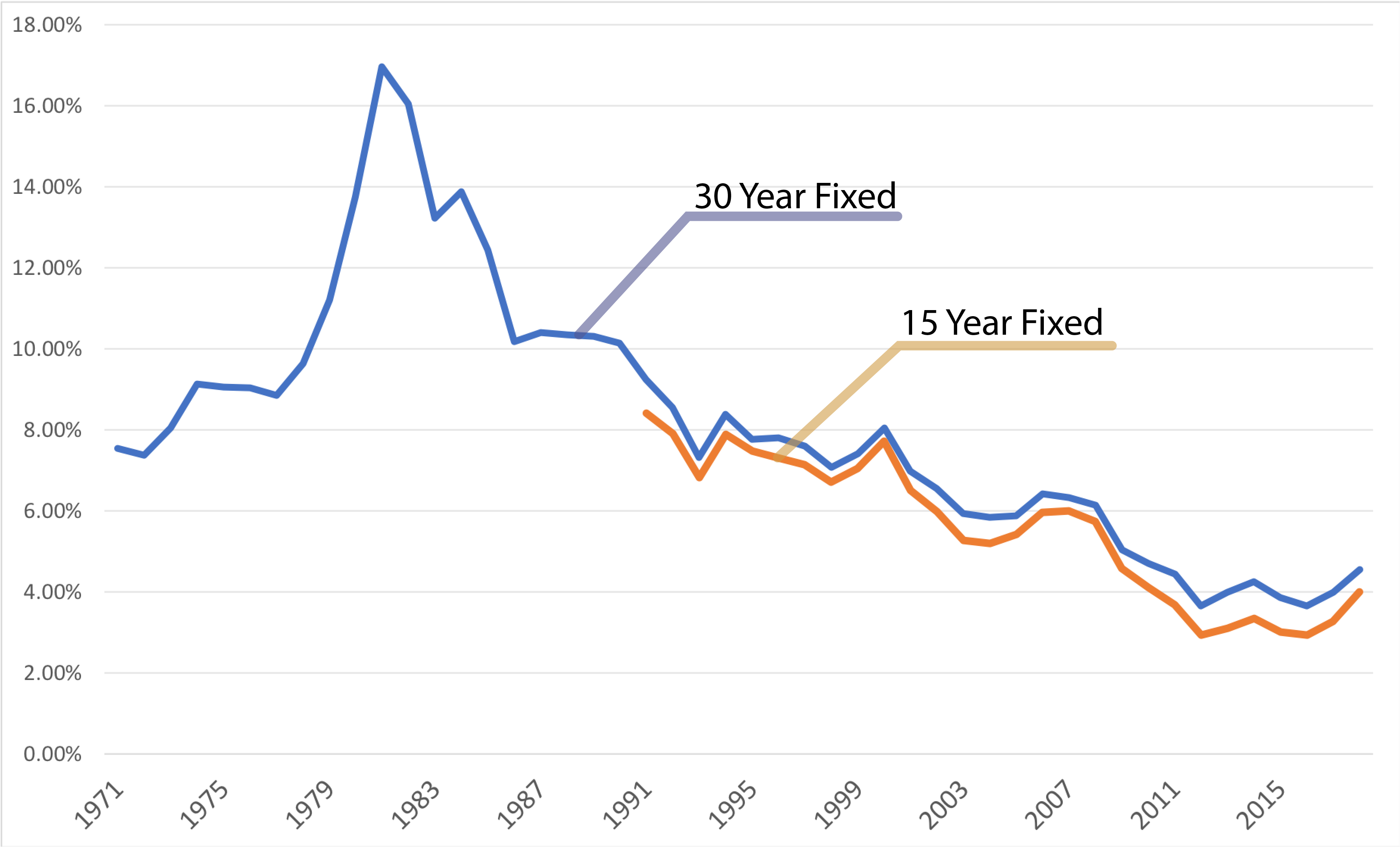

A home loan rates of interest a portion of your overall loan balance - what does ltv mean in mortgages. It's paid on a month-to-month basis, in addition to your primary payment, till your loan is settled. It's an element in identifying the annual cost to borrow money from a lender to buy a house or other property. Investors require higher interest rates to make back money when the economy, stock exchange, and foreign markets are strong. Bond investment activity can likewise affect mortgage rates, as well as your individual financial situation. However, you may have some options to decrease your lender's quoted interest rate when you're aiming to purchase a house. Your home mortgage rates of interest is what it costs you each month to finance your residential or commercial property. Your rate of interest is efficiently the lending institution's payment for letting you use its cash to buy your home. Mortgage rates of interest can vacillate depending on larger financial factors and investment activity. The secondary market plays a function. Fannie Mae and Freddie Mac bundle home loan and sell them to financiers looking to make a revenue. Mortgage Rates Decrease When The stock exchange falters. There are dips or insecurities in foreign markets. Inflation slows. Unemployment increases or jobs reduce. Mortgage Rates Increase When The stock market is strong. Foreign markets are strong and steady. Inflation is https://beterhbo.ning.com/profiles/blogs/some-of-what-is-the-interest-rate-today-on-mortgages up. why reverse mortgages are a bad idea. Joblessness is low and tasks are increasing. This chart shows how 30-year fixed-rate home loan rates altered from 2000 through 2019.

Top Guidelines Of What Will Happen To Mortgages If The Economy Collapses

The amount of interest you pay monthly will reduce as you settle the principal balance you obtained and as that number also decreases - what are reverse mortgages and how do they work. Your portion rates of interest applies to that staying balance. You'll pay 5% of your total loan balance in interest if you have a 5% home mortgage rate and you're making your first home loan payment. Is a percentage of the amount of cash you borrowed Is based upon your rates of interest, points, broker charges, and other costs. Can be found under "Loan Terms" on your loan quote Can be found under "Contrasts" on your loan price quote Is typically lower than your yearly portion rate since it's just one element of your APR Is usually higher than your home loan rate of interest Your interest rate is more of a total picture of just how much it costs you to borrow. As home loan rates rise, existing homeowners are less likely to list their residential or commercial properties and enter the market. This produces a lack of for-sale properties, driving demand up and rates with them. When rates are low, homeowners timeshareresalemarket.com reviews are more comfy offering their properties. This sends out inventory up and turns the marketplace in the purchaser's favor, indicating more choices and more negotiating power. It can suppress need if rates increase for too long or get too higheven for the timeshare store reviews the couple of properties that are out there. That would force sellers to decrease their prices in order to stick out. Rates vary by loan provider, so it's constantly crucial to search for the home loan loan provider that's offering the finest terms. Some Known Factual Statements About Why Reverse Mortgages Are A Bad Idea

In addition to market and economic elements, the rate you're offered depends largely by yourself monetary scenario. A loan provider will think about: Your credit ratingYour payment history and any collections, personal bankruptcies, or other monetary eventsYour earnings and work historyYour level of existing debtYour cash reserves and assetsThe size of your down paymentProperty locationLoan type, term, and quantity The riskier you are as a debtor and the more money you obtain, the higher your rate will be. Brokers can often find lower rates thanks to their industry connections and access to wholesale prices. Regardless of which path you choose, ensure you're comparing the complete loan estimateclosing expenses includedto properly see whose prices is more economical. You can usually pay discount points to lower the rate you're provided. One point equals 1% of the overall loan balance, and it reduces your rate of interest for the life of your mortgage. The amount it decreases your rate depends on your individual lender and the current market. This is often called "buying down your rate." Determine your break-even pointthe time it will consider you to recoup the costs of the points you purchasedto determine if this is the right move for you. A home mortgage interest rate is the percentage of your existing principal loan balance you pay your lending institution in exchange for borrowing the cash to purchase a residential or commercial property. It's not the like your interest rate (APR) which takes other costs, including your home loan rate of interest, into factor to consider. You'll normally pay a greater mortgage rate of interest if your credit is bad or if you have other negative financial issues. The Greatest Guide To What Is Today's Interest Rate For Mortgages

Utilize this tool throughout your homebuying procedure to check out the range of home loan rate of interest you can anticipate to receive. See how your credit rating, loan type, house cost, and down payment quantity can affect your rate. Knowing your options and what to expect helps make sure that you get a mortgage that is ideal for you. Remember that the rates of interest is very important, however not the only expense of a home loan. Costs, points, home loan insurance, and closing expenses all build up. Compare Loan Quotes to get the very best deal. Read Our Most Current "Daily Rate Update" Dec 16 2020, 4:36 PM Today marked the release of an updated policy declaration from the Federal Reserve. To put it simply, it was Fed day! Lots can occur on Fed days-- especially those that happen in December. This has progressively become a month where the Fed reveals an essential policy modification, or a minimum of a month where a Fed modification is ... Typical home mortgage rates inched lower yesterday, returning to the current all-time low. They've remained within a narrow range throughout this month, going up or down by a single basis point (one-hundredth of one percent) on all however two days., too. However there are a couple of: a Federal Reserve statement this afternoon, and any progress towards a pandemic relief plan in Washington D.C. The Best Strategy To Use For What You Need To Know About Mortgages

688% 2. 688% The same Conventional 15 year fixed 2. 375% 2. 375% Unchanged Conventional 5 year ARM 3% 2. 743% The same thirty years fixed FHA 2. 25% 3. 226% Unchanged 15 year repaired FHA 2. 25% 3. 191% The same 5 year ARM FHA 2. 5% 3. 226% Unchanged 30 year repaired VA 2. 295% Unchanged 15 year fixed VA 2. 063% 2. 382% Unchanged 5 year ARM VA 2. 5% 2. 406% Unchanged Rates are offered by our partner network, and might not show the marketplace. Your rate may be various. Click on this link for a customized rate quote. See our rate presumptions here. Elements that identify your home loan rate of interest include: A strong economy usually suggests higher rates, while a weaker one can press current home mortgage rates down to promote borrowing When a lending institution is really busy, it will increase rates to prevent brand-new service and provide its loan officers some breathing space (condo, single-family, townhouse, etc.) A primary home, suggesting a house you prepare to live in full-time, will have a lower rates of interest. The Buzz on What Percentage Of Mortgages Are Below $700.00 Per Month In The United States10/11/2021 If the applicant's credit rating was above a specific threshold, they were approved. Meanwhile, those with lower credit rating and maybe more engaging customer characteristics would be rejected. This led to a great deal of novice property buyers getting their hands on shiny new houses, even if their biggest loan prior had been something as basic as a revolving credit card. During the boom, these low home loan rates urged people to buy homes and serially re-finance, with numerous taking large amounts of cash-out in the procedure, typically every six months as house rates surged greater. A lot of these debtors had developed equity in their homes, however after pulling it out to pay everyday expenditures, had little left and nowhere to turn when funding dried up. Many of these customers now have loan quantities that far exceed the real worth of their houses, and a larger regular monthly mortgage payment to boot. Numerous of the houses lost during the crisis were really investment propertiesIronically, a lot of home loan and realty market employees participated the fun too and lost their hatsBut once again it didn't matter because they typically acquired the residential or commercial properties with nothing downAnd when things went south they merely walked away unscathedIt's not simply families who have actually lost their homes. Much of these speculators acquired handfuls of residential or commercial properties with little to no money down. Yes, there was a time when you might purchase four-unit non-owner occupied homes with no money down and no paperwork! Remarkable isn't it?Why loan providers ever thought that was a great concept is beyond me, however it occurred. There was absolutely a supply and need imbalanceJust too lots of homes out there and inadequate buyersEspecially when homes became too pricey and funding ran dryMany of these homes were also constructed in the borders where no one livedEverywhere you look, a minimum of if you reside in places like California, there are ratings of new, sprawling housing advancements. The smart Trick of How Common Are Principal Only Additional Payments Mortgages That Nobody is Discussing

Unfortunately, numerous were integrated in the outskirts of cities, often in places where many people do not really wish to reside. And even in preferable locations, the pace at which new residential or commercial properties were constructed significantly surpassed the demand to acquire the homes, triggering a glut of stock. The result was a heap of home builders going out of organization or hardly hanging on - what beyoncé and these billionaires have in common: massive mortgages.

Why? So they can discard off more of their houses to unwary households who believe they're getting a discount. Of course, the contractors don't actually wish to decrease house rates. They 'd rather Get more information the government subsidize rates of interest to keep their earnings margins intact. Everything worked because house costs kept risingBut they couldn't sustain permanently without imaginative financingAnd once rates stalled and began to dropThe flawed funding backing the residential or commercial properties was exposed in serious fashionAs an outcome of a number of the forces pointed out above, home costs increased rapidly. The pledge of nonstop house price gratitude hid the risk and kept the critics at bay. Even those who knew it would all end in tears were silenced because increasing house costs were the outright option to any problem. Heck, even if you could not make your month-to-month home loan payments, you 'd have the ability to sell your house for more than the purchase rate. Nobody was forced to buy a house or refinance their mortgageIt was all completely voluntary in spite of any pressure to do soWhat happened to all the money that was extracted from these homes?Ultimately everybody needs to take accountability for their actions in this situationFinally, the property owners themselves need to take some responsibility for what occurred. And where exactly did all this cash go? When you tap your equity, http://chancewapz427.hpage.com/post6.html you get money backed by a mortgage. But what was all that cash invested on? Were these equity-rich debtors purchasing brand brand-new vehicles, going on elegant trips, and buying a lot more real estate?The answer is YES, they were. Our Bonds Payment Orders, Mortgages And Other Debt Instruments Which Market Its PDFs

They were loans, not free money, yet lots of borrowers never paid the cash back. They just ignored their homes, however may have kept the numerous things they bought with the proceeds. You'll never ever hear anybody confess that though. Ultimately, each customer was responsible for paying their own mortgage, though there were certainly some bad players out there that might have manipulated a few of these folks. And while you can blame others for financial missteps, it's your issue at the end of the day so take it seriously. There are likely lots of more reasons behind the mortgage crisis, and I'll do my finest to add more as they come to mind. However this provides us something to chew on. Jonathan Swift It is clear to anyone who has actually studied the financial crisis of 2008 that the economic sector's drive for short-term revenue lagged it. More than 84 percent of the sub-prime home mortgages in 2006 were issued by personal loaning. These private companies made almost 83 percent of the subprime loans to low- and moderate-income debtors that year. The nonbank underwriters made more than 12 million subprime home loans with a worth of almost $2 trillion. The loan providers who made these were exempt from federal guidelines. How then might the Mayor of New York, Michael Bloomberg say the following at a business breakfast in mid-town Manhattan on November 1, 2011? It was not the banks that developed the home loan crisis. Now, I'm not saying I make certain that was horrible policy, because a great deal of those people who got houses still have them and they wouldn't have gotten them without that. However they were the ones who pushed Fannie and Freddie to make a lot of loans that were unwise, if you will - who took over abn amro mortgages. Get This Report about What Kind Of Mortgages Do I Need To Buy Rental Properties?

And now we wish to go Visit this website vilify the banks because it's one target, it's simple to blame them and Congress definitely isn't going to blame themselves." Barry Ritholtz in the Washington Post calls the notion that the US Congress was behind the financial crisis of 2008 "the Big Lie". As we have actually seen in other contexts, if a lie is huge enough, people begin to think it. Bear in mind that rates alter daily, so you'll want to be sure you have the right loan provider prior to you secure a rate and complete the application. Also inquire about points, which are charges that might permit you to get a lower interest rate. Learn how much they cost and whether you need them at all. Not all of them are clearly reasonable. Some lenders may note the fees individually while others lump them how to get out of my timeshare together. Ask about all of themincluding application charges, underwriting costs and others that are charged at closing. Compare between lenders and work out as a lot of the costs as possible. You'll desire to put down as much money as possible on a home loan, however likewise ensure you're conserving for the inevitable house expensessuch as repairs and furnishingsfor when you move in. If you put down less than 20%, you'll likely need to pay personal home loan insurance (PMI). Once you choose which offer is finest for you, complete the application. As long as you have your documents in order and there aren't any monetary problems that occur before closing day, you have actually likely been through the most difficult part of the home mortgage procedure. In basic, the conforming loan limit for 2020 is $510,400, which indicates that any amount over that will have to be obtained with a jumbo loan. FHA loan limitations for 2020, on the other hand, range from $331,760 to $765,600, but your particular maximum will depend upon the location you live in and other factors.

Otherwise, it's anyone's guess. Discount points are generally a charge you pay to your lending institution that enables you to decrease the interest rate on your loan. You can purchase these points if you want a lower rate of interest but can't certify or rates just aren't that low presently. In general, each discount point will cost you about 1% of the primary amount of your loan, so the cost for discount rate points can accumulate quickly particularly with larger loan quantities. Some Of What Is The Current Apr For Mortgages

Each discount point you acquire reduces your loan's interest rate by anywhere from 1/8 to 1/4 of a percent, so you might be paying more than you're saving. Each scenario is unique, though and you won't understand whether the discount points make sense up until you do the calculations with your loan rate and principal (what are the best banks for mortgages). Lenders provide a wide range of loan types and rates, and the only method to understand what you receive is to compare the offers. Do not mark down smaller credit unions or online lending institutions, either especially if you have a relationship with one currently. Credit unions are an excellent location to discover extremely low home mortgage rates, however they need you to be a member of the CU and you frequently require to develop a relationship with them prior to they'll provide those rates to you. Getting the very best home loan rate also involves a solid monetary profile. If you have credit or financial concerns, you won't be used the most affordable rates no matter how much you shop around. So be sure to get your money ducks in a row prior to you look for any loans.Mortgage closing expenses are any extra charges you pay for your mortgage aside from the loan principal and interest. For example, if you have an interest in a$ 350,000 house, the closing expenses would range from$ 7,000 to$ 17,500. The charges cover experts and services needed to settle your home buying process. These closing costs cover a few charges, including the home appraisal to assess the worth of your brand-new home and in some cases, a credit reporting charge to cover the cost of reviewing your credit. Often, experts highly advise negotiating lending institution service expenses consisting of application costs or any costs you do not recognize. You can likewise ask about consisting of some closing costs into your loan, but this choice might suggest a higher interest rate. You won't be able to negotiate a few of the closing cost charges, consisting of taxes or title insurance coverage required by the lender, but there are a few charges you can decrease or ask the buyer to cover. How can I save money on home mortgage interest rates?Work on your credit rating: The much better ball game, the lower threat you will be to a lender, which will offer you access to much better rates of interest. Secure a mortgage with your existing bank: While your bank might not provide the most affordable rate of interest, you may get lucky and be offered an unique rate for being an existing customer. When should you re-finance your mortgage?Refinancing is when you replace your home loan with a new one. This is often done after. you have actually constructed up a better credit rating and can get approved Go to this website for lower rates of interest westlake financial group inc or have a higher income and shorten your loan with greater month-to-month payments. By changing the older loan, you can decrease your monthly payments and the total expense you pay to obtain the money. When refinancing, you can likewise lower the length of your loan and eliminate personal mortgage interest. More About What Was The Impact Of Subprime Mortgages On The Economy

You may also desire to refinance to change your loan from a variable-rate mortgage to a fixed-rate mortgage depending on the rate of interest you're currently paying. How do you compare various types of home mortgage lendersWhile you're looking for the very best possible mortgage rate and home mortgage type, take into account the various types of home loan lenders on the marketplace today. We've narrowed home loan loan providers into three categories: This category consists of home loan lenders that work for the major banking institutions( Bank of America, Wells Fargo, and so on). Home loan lenders can supply direct links between lending institutions and the organizations that supply the capital for their home mortgage. There's more security in utilizing a mortgage lender, and if you currently have an excellent history with the bank, you may be able to obtain a lower rates of interest than on the marketplace.Mortgage brokers are essentially intermediaries between debtors and loan providers. Credit unions can be an appealing choice for anybody looking to find a home mortgage with average to bad credit. They tend to run as nonprofits and tend to keep loans internal rather than utilizing 3rd celebrations. Non-bank lenders, such as Quicken Loans, concentrate on home mortgages and don't use other traditional customer banking services. Mortgage insurance coverage can offer protection for your loan provider but it isn't constantly necessary. (iStock) Prepared to purchase your very first house!.?.!? When determining what you can manage to invest on a home, home mortgage insurance coverage is an essential number you require to consider. Home loan insurance may be needed to get a home mortgage, depending upon the size of your down payment and which type of mortgage you're getting. Whether you ought to get home loan insurance or will be required to have it, depends upon the regards to your loan. If you're purchasing a home with a standard home loan, for example, you 'd likely require to pay private mortgage insurance coverage (PMI) if your down payment is less than 20 percent of the purchase rate. The real premium you pay depends on the loan type, loan terms, and your danger level, stated Matthew Posey, a certified home mortgage preparation expert with Axia Home Loans. This type of insurance is different than home mortgage protection insurance or mortgage life insurance coverage. This type of home loan insurance covers you, not the lending institution, and purchasing a policy is optional. For instance, if you can't make your payments due to the fact that of a task loss, disease or any other reason, this coverage starts and enables your home loan lending institution to recover losses if the house has actually to be offered in a foreclosure proceeding. Essentially, you're paying money on top of your regular mortgage payment to make sure the loan provider has a safeguard if you can't make great on your loan. Blank Have Criminal Content When Hacking Regarding Mortgages Can Be Fun For Anyone

Mortgage defense insurance covers you and assists to pay off your mortgage if you become handicapped or pass away. So if you were to drop dead, any remaining amount owed on your house loan would be settled. The policy's protection diminishes as your mortgage balance goes down, so it's not the like a conventional life insurance coverage policy. Might assist with your eligibility for a home loan if you can't pay for a bank's 20 percent deposit requirements. PMI on traditional loans can be canceled once you reach 20 percent equity in the home - why is there a tax on mortgages in florida?. Mortgage life insurance policies can assist your liked ones remain in the home if something occurs to you. Home loan life insurance may provide less coverage and a higher expense compared to standard life insurance coverage. Home loan life insurance policies might feature various exceptions in which your protection wouldn't apply. One extra benefit of having home mortgage insurance coverage is best timeshare cancellation company the potential to get a lower interest rate. "The rate supplied will typically be lower because the home loan insurance coverage protects the loan provider, thus alleviating a few of the threat within the loan," Posey stated. That may be simpler said than done, however, if you're attempting to conserve for a house while also paying for trainee loans or other financial obligations. In that case, it may be valuable to consider alternative methods to raise the deposit money you require. For instance, you might consider: Deposit assistance programs offer aid with down payments and closing expenses for qualified buyers. How Much Is Mortgage Tax In Nyc For Mortgages Over 500000:oo Fundamentals Explained

You can withdraw approximately $10,000 from an Individual Retirement Account towards the purchase of a first home penalty-free. Considering that mortgage life insurance coverage is optional, there's absolutely nothing unique you require to do to avoid it. However if you're thinking about buying a policy, compare the cost and protection to a regular life insurance policy initially to see which one might yield more benefits. Veterans' Home Mortgage Life Insurance Coverage (VMLI) is mortgage defense insurance coverage that can assist families of badly timeshare meetings handicapped Servicemembers or Veterans settle the house mortgage in the event of their death. Please download the VMLI sales brochure for general info about the Veterans Home Loan Life Insurance Coverage Program. VMLI is only readily available to Servicemembers and Veterans with serious service-connected disabilities who: Gotten Specifically Adapted Real Estate (SAH) grant to assist build, redesign, or acquire a house, Have the title to the home, Have a mortgage on the house Veterans must get VMLI before their 70th birthday. e., a bank or home mortgage loan provider), not to a recipient. The quantity of coverage will equal the quantity of the home mortgage still owed, but the maximum can never ever surpass $200,000. VMLI is reducing term insurance coverage which lowers as the mortgage balance decreases. VMLI has no loan or money values and does not pay dividends. The Specifically Adjusted Housing Representative will assist the Servicemember or Veteran complete VA Kind 29-8636, Application for Veterans' Home Mortgage Life Insurance (when does bay county property appraiser mortgages). If a Servicemember or Veteran does not get VMLI coverage at that time, VA will send out a letter informing them that they are qualified for such coverage. In addition to completing VA Form 29-8636, the Servicemember or Veteran need to offer details about their present home mortgage. Our How Does Bank Know You Have Mutiple Fha Mortgages Diaries

It's a property owner's nightmare: Ending up being ill enough that you can no longer work, possibly causing you to miss out on house payments and lose your home. While homeowner's insurance coverage secures you against fire, weather damage and theft, it does not protect you if you are not able to pay your home loan every month - how is mortgages priority determined by recording. For anyone with a mortgage, homeowner's insurance is compulsory. It's developed to help ensure the home keeps its worth, securing you and the loan provider. House owner policies vary from one state to another, but in general, they cover fire, downed trees, vandalism, broken water pipelines, storms and wind. If anyone is hurt on your property, that's covered, too. What's not covered, nevertheless, is your actual home loan. Should you get ill and be unable to work, or lose your job, you would require to have other kinds of insurance protection. Simply as the name suggests, home mortgage security insurance is designed to secure your mortgage in case you can't pay. Mortgage protection insurance coverage is normally issued on wesley financial group complaints a "ensured acceptance" basis-- a significant benefit for somebody who has existing health concerns or works in a high-risk occupation. Home mortgage defense insurance can be paid as a separate bill, much like automobile insurance, or it can be infiltrated your monthly mortgage payment.

The 8-Second Trick For What Do I Need To Know About Mortgages And Rates

Depending on the policy, impairment insurance typically pays 60 percent of your month-to-month salary for a set time, which might vary from six months to a maximum of two years. The majority of group strategies-- the type you receive from your company-- have a cap on how much will be paid, such as $5,000 per month or $60,000 annually. If you are self-employed or your employer does not supply long-term impairment insurance, you can acquire a specific plan that works much the very same. And even if your company does supply it, you can also purchase additional protection that will insure as much as 20 percent more of your earnings. Depending upon your circumstance, that 20 percent additional can indicate real assurance. MPI is a great choice for some homeowners however not the very best option for others. Let's compare the benefits and drawbacks before seeing if it's best for you. MPI has actually proven to be beneficial for lots of house owners. One advantage of MPI is that it has actually ensured acceptance. This indicates that property owners do not need to pass a health exam to fulfill underwriting requirements for either death or special needs benefits. HECM loans typically must be settled when the last borrower dies, sells, or completely relocates from the house. Considering that August 4, 2014, the HECM loan documents explicitly permit a non-borrowing spouse to stay in the house after the borrower's death, till the non-borrowing partner either dies or vacates.

HUD developed the Mortgagee Optional Election (MOE) to permit non-borrowing partners with pre-August 2014 loans to remain in your home after the customer dies if they fulfill the eligibility requirements and continue to meet the terms of the loan. Under the modified guidelines issued September 2019, non-borrowing partners no longer need to supply proof of valuable title or a legal right to remain in the home. The brand-new policy unwinds program deadlines and requires servicers to alert debtors about the existence of the option and demand the names of partners who may potentially get approved for the choice. Customers will receive the notice and kind with the yearly tenancy certification. The reverse mortgage lending institution is not required to offer a MOE to a non-borrowing partner. To prevent being financially penalized, a lender should choose the MOE alternative within a reasonable duration, typically within 180 days of the death of the debtor. This duration is momentarily extended due to the pandemic. Lenders may pick the MOE alternative even after starting the foreclosure process. A making it through non-borrowing spouse who is provided the MOE should establish eligibility under the program's standards. If the borrower was enrolled in a strategy to repay property charge financial obligations, the non-borrowing spouse must bring the delinquency as much as date before the lender appoints the loan to HUD. If the non-borrowing partner gets approved for the MOE, the due and payable status on the loan will be postponed and the loan will not be subject to foreclosure up until the spouse moves out of the home, dies, or stops working to satisfy the conditions of the loan. 4 Simple Techniques For How To Add Dishcarge Of Mortgages On A Resume

Debtors with a reverse mortgage should pay property-related charges including property tax, risk and flood insurance coverage premiums and, if appropriate, HOA charges, condo association costs, ground rents, or other special evaluations. Lenders may utilize different choices to deal with home charge defaults. Despite the menu of options, lending institutions can exercise their discretion and refuse to offer any of the noted below: Payment Strategies: Repayment plans of 60 months or less are offered based upon the debtor's surplus earnings. e., taxes and insurance) due over the next 90 days. In some circumstances, repayment plans can be renegotiated if the borrower suffers a brand-new hardship or once again stops working to pay residential or commercial property charges. At Threat Extensions: Borrowers 80 years Click for source or older might receive an "at risk extension" of the foreclosure timeframe if they satisfy particular crucial conditions such as struggling with a terminal disease, long-lasting handicap or a distinct tenancy requirement (i. terminal health problem of a family member getting care at the home) (how many mortgages in one fannie mae). HUD must authorize this extension, which is restored every year. Delay calling the loan due for a low amount of home charge defaults: If the residential or commercial property tax and insurance defaults are less than $2,000, lenders can delay calling the loan due while they deal with the borrower to get captured up. Lending Institution Payment of Outstanding Residential Or Commercial Property Charges: Lenders may use their own funds to pay a customer's outstanding property charges however they are not permitted to add that amount to the loan balance or look for repayment from HUD. They likewise undergo other restrictions. what is the best rate for mortgages. A borrower might pay off exceptional residential or commercial property charges such as real estate tax and insurance coverage at any time, even after foreclosure proceedings have begun, and the loan will be reinstated, based on particular limitations. Direct aid from nonprofit companies and state government might likewise assist delinquent customers, where available. Support may be available from a HUD-approved real estate therapy company to access these alternatives. A reverse home loan might be called due and payable if the home is not the primary house of a minimum of one customer for longer than 12 successive months. An Unbiased andrew reinhart View of Percentage Of Applicants Who Are Denied Mortgages By Income Level And Race

Non-borrowing partners who got approved for a deferment of foreclosure should likewise provide an accreditation of occupancy. HUD has actually taken steps to temporarily relieve documents requirements throughout the COVID-19 pandemic by enabling an e-mail or spoken certification from the debtor. Unfortunately, lots of lenders may still rely on the signed tenancy certification or fail to take additional steps to verify tenancy of the house. Federally-insured HECM reverse home mortgages allow older homeowners to utilize the equity in their home as resource to age in location. Regrettably, an increasing variety of older homeowners are defaulting under the regards to the home mortgage and dealing with foreclosure and eviction from their home. This pattern is likely to worsen as older house owners handle the fallout from the COVID-19 pandemic - how is mortgages priority determined by recording. U.S. Department of Housing and Urban Development (HUD): www. hud.gov Discover a HUD-approved real estate counseling company: www. hudexchange.info/ programs/housing-counseling/customer-service-feedback HECM for Lenders Site with copies of HECM policy, design forms, Handbook and Mortgagee Letters: https://www. hud.gov/ program_offices/ housing/sfh/hecm Real estate Therapy & National Advocacy Organizations Senior Homeownership Preservation Job (SHOPP): (773) 262-7801. This job works with HECM debtors who are dealing with default on their mortgages due to non-payment of residential or commercial property taxes or homeowners insurance. nclc.org Legal Assistance Legal services/ Legal aid: www. lsc.gov/ what-legal-aid/find-legal-aid Volunteer legal representatives: www. americanbar.org/groups/legal_services/flh-home/flh-free-legal-help. html National Association of Consumer Supporters: www. naca.net Publications National Customer Law Center, Home Foreclosures (1st ed. 2019) National Customer Law Center, Mortgage Loaning (2019 3rd ed.) The Revised HECM Financial Evaluation and Residential Or Commercial Property Charge Guide is readily available as an attachment to Mortgagee Letter 2016-10 (July 13, 2016) at https://www. Government Responsibility Office, "Reverse Mortgages: http://zandertnjg012.wpsuo.com/the-single-strategy-to-use-for-how-do-reverse-mortgages-really-work FHA Requirements to Enhance Monitoring and Oversight of Loan Outcomes and Maintenance," (September 2019), readily available at: https://www. gao.gov/ assets/710/701676. pdf. Federally backed loans are those where Fannie Mae or Freddie Mac is the investor or where the Federal Housing Administration (FHA), Veterans Affairs (VA), or the U.S. Little Known Questions About What Banks Give Mortgages Without Tax Returns.

This protection does not apply to exclusive reverse home loans, unless Fannie Mae is the investor. U.S. Department of Housing and Urban Advancement, Mortgagee Letter 2020-04, March 18, 2020. U.S. Department of Real Estate and Urban Advancement, Mortgagee Letter 2020-06, April 1, 2020. U.S. Department of Housing and Urban Advancement, Mortgagee Letter 2019-15, Sept. U.S. Department of Housing and Urban Advancement, Mortgagee Letter 2020-12, April 14, 2020. Odette Williamson, a lawyer with the National Customer Law Center, concentrates on real estate sustainability, issues affecting older adults, and directs the Racial Justice and Equal Economic Chance initiative. She is co-author of NCLC's manuals on foreclosures and home mortgage servicing. In some cases, fraudster mortgage lenders and brokers tell elderly homeowners that they can use a reverse home loan to stop an upcoming foreclosure which reverse mortgages themselves do not ever get foreclosedbut this simply isn't real. While in many cases getting a reverse home mortgage might be a great way to stop a foreclosure, it's normally a bad concept. Keep checking out to discover the fundamentals about reverse home loans, how getting a reverse home mortgage can stop a foreclosure, why securing a reverse mortgage for this function typically isn't a good concept, and other options to think about rather. With a routine home mortgage, a person borrows a lump amount of money and pays the loan provider back in time, generally by making regular monthly payments. PMI and Check over here MIP represent personal home mortgage insurance coverage and home mortgage insurance premium, respectively. Both of these are kinds of mortgage insurance to protect the lending institution and/or investor of a home mortgage. If you make a deposit of less than 20%, home loan investors implement a home mortgage insurance coverage requirement. In many cases, it can increase your monthly payment of your loan, but the flipside is that you can pay less on your deposit. FHA loans have MIP, that includes both an in advance home loan insurance premium (can be paid at closing or rolled into the loan) and a monthly premium that lasts for the life of the loan if you only make the minimum down payment at closing. Getting prequalified is the primary step in the mortgage approval procedure. However, given that earnings and Click here! possessions aren't verified, it just serves as a quote. Seller concessions involve a provision in your purchase agreement in which the seller consents to aid with specific closing expenses. Sellers might consent to spend for things like real estate tax, lawyer charges, the origination charge, title insurance and appraisal. Payments are made on these bills when they come due. It utilized to be that banks would hold on to loans for the entire regard to the loan, however that's progressively less typical today, and now the majority of mortgage are offered to among the major mortgage investors believe Fannie Mae, Freddie Mac, FHA, etc. Quicken Loans services most loans. A home title is evidence of ownership that likewise has a physical description of the house and land you're purchasing. The title will also have any liens that give others a right to the residential or commercial property in specific situations. The chain of title will show the ownership history of a particular home. What Are The Different Types Of Home Mortgages - Truths

Home mortgage underwriting is a stage of the origination process where the loan provider works to confirm your income and property info, debt, along with any home information to release final approval of the loan. It's basically a process to evaluate the amount of threat that is associated with providing you a loan. With validated approval, your deal will have equivalent strength to that of a money buyer. The procedure starts with the exact same credit pull as other approval stages, however you'll also need to offer documents consisting of W-2s or other earnings confirmation and bank declarations. Forbearance is when your mortgage servicer or lender enables you to stop briefly (suspend) or minimize your home loan payments for a limited duration of time while you restore your financial footing. The CARES Act provides numerous homeowners with the right to have all home loan payments completely paused for a period of time. You are still needed to pay back any missed out on or minimized payments in the future, which most of the times may be paid back over time. At the end of the forbearance, your servicer will contact you about how the missed out on payments will be repaid. There might be various programs offered. Make certain you comprehend how the forbearance will be repaid. For example, if you have a Fannie Mae, Freddie Mac, FHA, VA, or USDA loan, you won't need to pay back the quantity that was suspended all at onceunless you have the ability to do so. If your income is restored before completion of your forbearance, reach out to your servicer and resume making payments as quickly as you can so westlake financial group inc your future responsibility is limited. What Is The Going Interest Rate On Mortgages for Dummies

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. Nevertheless, this does not affect our evaluations. Our viewpoints are our own. You've decided to purchase a house. Take a huge breath it's not every day you look for a loan with that many zeros. Preparation is key, since after your purchase offer is accepted, the clock is ticking. Closing a home loan transaction takes about 45 days usually. "If you get in into the procedure without [the correct] information, it could slow you down," states Randy Hopper, a vice president at Navy Federal Credit Union. Now that you've made a deal on a home, it's time to pick the finalist that you will actually borrow the money from. Start by phoning lending institutions (three, at minimum), visiting their workplaces or submitting their home mortgage applications online. Easiest of all: Ask an agent to submit the form while you supply details by phone or face to face, states Carlos Miramontez, vice president of mortgage lending at Orange County's Credit Union in California. Mark Burrage, USAA "If you want to begin online, and you get to the point where you need more details or just desire to talk with a live person, the vast bulk of lending institutions are established to where you can funnel switch," says Mark Burrage, an executive director for USAA (what credit score do banks use for mortgages). And your credit rating won't experience sending multiple applications as long as you submit them all within a 45-day window. You need to constantly send multiple applications so you can compare deals later on. It's a good concept to work with a house inspector to assess the home's condition immediately, although lending institutions don't need it. The Buzz on What The Interest Rate On Mortgages Today

This will cost around $300 to $500. The lending institutions ask permission to pull your credit. By law, a loan provider has 3 organization days after receiving your application to offer you a Loan Estimate form, an in-depth disclosure showing the loan quantity, type, rates of interest and all costs of the home loan, consisting of threat insurance coverage, home mortgage insurance, closing costs and residential or commercial property tax. Now utilize your Loan Quote forms to compare terms and costs. At the upper right corner of the very first page you'll see expiration dates for the interest rate discover out if it's "locked" and closing costs. Ask the lending institution to describe anything you do not comprehend. If the numbers seem excessive, "Do not focus excessive on rate," Burrage states. These will allow you to quickly compare deals: This is all charges including interest, principal and home mortgage insurance coverage that you'll sustain within the home mortgage's very first 5 years. This is the amount of principal you'll have settled in the very first five years. Also called its interest rate. This is the percentage of the loan paid in interest over the whole life of the mortgage. The lender's task is to respond to all your questions. If you can't get excellent responses, keep shopping. [Back to top] You've compared lenders' rates and fees. Now examine their responsiveness and credibility. Think two times about anyone who makes you feel forced, Burrage states. His guidance: "Opt for somebody you can trust." Then call the lending institution of your option to state you're prepared to proceed. Editorial Note: Forbes might make a commission on sales made from partner links on this page, but that does not affect our editors' opinions or examinations. Just weeks prior to the new year, home loan rates are breaking records yet once again. Mortgage rates on the 30-year fixed-rate home loan fell to their floor for the 14th time this year, slipping to 2. The brand-new record may be a little a surprise, as the bond market perked up on Tuesday following murmurs of fiscal relief. Treasury yields, which usually move in tandem with mortgage rates, increased a little, but did not bring home loan rates with them. With home loans in high need and the refinance share of home mortgage applications up 102% year-over-year, lending institution revenues are skyrocketing, according to a recent report by the Mortgage Bankers Association. This, combined with an aggressive fiscal policy from the Federal Reserve, is what's keeping a cover on rates. "The Federal Reserve's anticipated strategies to continue their rate of mortgage-backed securities purchases is also most likely to keep upward movements in home mortgage rates in check," says Matthew Speakman, an economist at Zillow. Mortgages to purchase a home were up 9% week-over-week, after changing for the Thanksgiving vacation, and were 28% greater than the exact same time in 2015, according to the Home loan Bankers Association's (MBA) Weekly Mortgage Applications Survey for the week ending Nov. 27, 2020. The serious housing shortage has pushed the average purchase loan total up to $375,000, the greatest level considering that MBA began its study in 1990. "The continual duration of low home loan rates continues to stimulate borrower need, and the mortgage industry is poised for its strongest year in originations given that 2003," states Joel Kan, associate vice president of economic and industry forecasting for MBA. "The ongoing refinance wave has been useful to homeowners wanting to decrease their regular monthly payments during these challenging financial times produced by the pandemic." The typical rate for the benchmark 30-year repaired dropped one basis indicate 2. Excitement About Who Has The Best Interest Rates For Mortgages

A basis point is one one-hundredth of a portion point. This time last year, the 30-year repaired was 3. 68%. Customers with a 30-year fixed-rate home mortgage of $300,000 with today's rate of interest of 2. 71% will pay $1,218. 38 each month in principal and interest (taxes and costs not included), the Forbes Consultant home loan calculator programs. 60. That very same home loan gotten a year ago would cost an extra $57,269. 11 in interest over the life of the loan. The average rate of interest on the 15-year set home mortgage dropped two basis points last week to 2. 26%. This time in 2015, the 15-year fixed-rate home mortgage was at 3. Debtors with a 15-year fixed-rate home loan of $300,000 with today's rate of interest of 2. 26% will pay $1,966. 65 each month in principal and interest (taxes and costs not included). The overall interest paid over the life of the loan will be $53,997. 26. The typical rate on a 5/1 adjustable-rate mortgage fell 30 basis points to 2.

16% last week. how many mortgages in the us. In 2015, the 5/1 ARM was 3. 39%. ARMs are house loans that have a rate of interest that fluctuates with the marketplace. In the case of 5/1 ARMs, the first 5 years have a set rate and after that change to a variable rate after that. That indicates when the average rate increases or falls, so will your rate. Home mortgage rates are at record lows, so this might be a suitable time for lots of folks who wish to conserve money on their home mortgage or refinance their existing home mortgage. If you're refinancing, understand you may pay a slightly greater rate of interest since of a new refinancing charge. Customers who wish to get the least expensive rate ought to ensure they have a credit report of at least 760. Not known Details About What Are The Current Refinance Rates For Mortgages

In reality, debtors with lower credit history can be charged one portion point or more greater than customers with excellent or outstanding scores. Prior to you request a home mortgage, examine your credit score. Numerous banks and credit cards permit you to do this free of charge. One way you can improve your rating reasonably quickly is to pay for financial obligation. In addition to your credit rating, loan providers will look at your debt-to-income ratio, or DTI. This is your total regular monthly debt divided by your gross regular monthly earnings. It's essentially a photo of just how much you owe versus just how much you earn. The lower your DTI, the much better opportunities you have of getting a lower rates of interest. Lastly, research studies have shown that individuals who look around tend to get lower rates than those who get a mortgage from the very first lending institution they talk to. Know what the existing average rate of interest is as well as what your credit score, earnings, financial obligation and expenditures are prior to you start using. As the Federal Reserve concludes a two-day conference Wednesday, it will be fighting with how to respond to opposing forces in the country's COVID-19-fueled financial crisis. On the one hand, a revival of the virus already has actually slowed the economy and an even darker winter season lays ahead. At the exact same time, broad schedule of a vaccine by spring provides the prospect of a substantial enhancement. However Fed officials still have more ammo, mostly associated to their enormous bond-buying stimulus targeted at holding down long-term rates that impact mortgages and other loans. The Fed's policy choice, which will be launched at 2 p. m. on Wednesday, is expected to center around those bond purchases-- and it could imply a little lower monthly costs for property buyers and other customers. What Do Underwriters Do For Mortgages - Questions

Here's the breakdown of what the Fed may do: The Fed is now purchasing $80 billion in Treasury bonds and $40 billion in mortgage-backed securities each month, putting down pressure on long-lasting rate of interest, such as for home loans and business bonds. The typical maturity of the securities it's purchasing is 7. Some economic experts anticipate Fed officials to buy the exact same amount of bonds but shift the mix towards those with longer maturities. That would inject more stimulus into the economy by more pressing down rates for home loans, business bonds and other types of loans. COVID-19 is spiking across the country, with cases, hospitalizations and deaths reaching brand-new records. Task development slowed greatly in November and initial out of work claims, a rough measure of layoffs, jumped greatly to 947,000 the week ending December 5."The economy actually requires," more stimulus, states Oxford economist Kathy Bostjancic. "Fed authorities may see the winter season infection Click here for info revival as the obvious moment to shoot their last bullet," Goldman Sachs stated in a research note. This produces a tidal wave of brand-new work for mortgage lending institutions. Unfortunately, some lending institutions don't have the capability or manpower to process a large number of refinance loan applications. In this case, a lending institution might raise its rates to hinder brand-new company and give loan officers time to process loans currently in the pipeline. Cash-out refinances position a greater danger for home mortgage lending institutions, so they're typically priced higher than brand-new home purchases and rate-term refinances. Considering that rates can differ, always go shopping around when buying a house or re-financing a mortgage. Window shopping can potentially conserve thousands, even tens of thousands of dollars over the life of your loan. Some just opt for the bank they utilize for checking and savings because that can appear most convenient. However, your bank may not use the finest home loan deal for you. And if you're re-financing, your monetary scenario might have altered enough that your current lender is no longer your best option. The 10-Minute Rule for How Many Mortgages Can You Have At One Time

When looking for a home loan or re-finance, lenders will provide a Loan Price quote that breaks down important costs associated with the loan. You'll wish to check out these Loan Price quotes carefully and compare costs and charges line-by-line, consisting of: Interest rate Annual portion rate (APR) Monthly mortgage payment Loan origination fees Rate lock fees Closing costs Remember, the most affordable rates of interest isn't constantly the very best offer. It approximates your overall yearly cost consisting of interest and charges. Also pay attention to your closing expenses. Some loan providers may bring their rates down by charging more upfront through discount points. These can include thousands to your out-of-pocket expenses. You can likewise negotiate your home mortgage rate to get a better offer (how do down payments work on mortgages). Lender An offers the much better rate, however you choose your loan terms from Lender B. Talk With Lending institution B and see if they can beat the former's prices. You may be shocked to discover that a lender is prepared to provide you a lower interest rate in order to keep your service. Mortgage debtors can choose in between a fixed-rate home mortgage and an variable-rate mortgage (ARM). Fixed-rate home mortgages (FRMs) have rates of interest that never ever change, unless you decide to refinance. This results in predictable month-to-month payments and stability over the life of your loan. Adjustable-rate loans have a low interest rate that's repaired for a set variety of years (usually five or seven). With each rate adjustment, a customer's mortgage rate can either increase, decrease, or stay the very same. These loans are unforeseeable since regular monthly payments can change each year. Variable-rate mortgages are fitting for debtors who anticipate to move prior to their very first rate change, or who can manage a higher future payment. What Is The Current Interest Rate On Reverse Mortgages Fundamentals Explained

Keep in mind, if rates drop sharply, you are complimentary to re-finance and secure a lower rate and payment later. You don't need a high credit history to receive a home purchase or re-finance, but your credit rating will impact your rate. This is since credit report determines risk level. For the very best rate, aim for a credit report of 720 or greater. Home mortgage programs that don't require a high score consist of: minimum 620 credit rating minimum 500 credit history (with a 10% deposit) or 580 (with a 3. 5% down payment) no minimum credit rating, but 620 is common minimum 640 credit rating Ideally, you desire to inspect your credit report and score at least 6 months before requesting a Helpful hints home mortgage. If you're all set to use now, it's still worth inspecting so you Click here for more have a great concept of what loan programs you might get approved for and how your rating will impact your rate. You can get your credit report from AnnualCreditReport. com and your score from MyFico. com. Nowadays, home mortgage programs don't need the conventional 20 percent down. Down payment minimums differ depending on the loan program. For instance: need a down payment in between 3% and 5% require 3. 5% down permit zero down payment generally need a minimum of 5% to 10% down Keep in mind, a greater deposit lowers your danger as a borrower and helps you work out a better home mortgage rate. This is an included cost paid by the borrower, which protects their loan provider in case of default or foreclosure. However a huge down payment is not needed. For lots of people, it makes good sense to make a smaller deposit in order to buy a house quicker and begin developing house equity. 7 Simple Techniques For What Is The Current Index Rate For Mortgages

The 5 primary kinds of home loans include: Your interest rate remains the same over the life of the loan. This is a great alternative for debtors who expect to live in their houses long-term. The most popular loan alternative is the 30-year home loan, however 15- and 20-year terms are likewise typically readily available. Then, your home mortgage rate resets every year. Your rate and payment can increase or fall every year depending upon how the broader interest rate patterns. ARMs are ideal for debtors who expect to move prior to their first rate adjustment (typically in 5 or 7 years). For those who prepare to remain in their house long-lasting, a fixed-rate home loan is usually suggested. In 2020, the conforming loan limit is $510,400 in many areas. Jumbo loans are ideal for debtors who need a larger loan to buy a pricey property, especially in big cities with high genuine estate values. A federal government loan backed by the Federal Housing Administration for low- to moderate-income debtors. A federal government loan backed by the Department of Veterans Affairs. To be eligible, you need to be active-duty military, a veteran, a Reservist or National Guard service member, or an eligible partner. VA loans allow no deposit and have exceptionally low home loan rates. USDA loans are a government program backed by the U.S. They use a no-down-payment solution for borrowers who acquire real estate in a qualified rural area. To qualify, your earnings must be at or listed below the local mean. Debtors can receive a home mortgage without income tax return, utilizing their personal or company checking account. This is an option for self-employed or seasonally-employed customers. An Unbiased View of How Many Home Mortgages In The Us

This gives lenders the flexibility to set their own guidelines. Non-QM loans might have lower credit rating requirements, or deal low-down-payment choices without home loan insurance. The lending institution or loan program that's right for someone may not be right for another. Explore your options and then choose a loan based upon your credit rating, down payment, and monetary objectives, in addition to local house prices. Usually, it only takes a few hours to get quotes from multiple lending institutions and it could conserve you thousands in the long run. We receive existing home mortgage rates every day from a network of home loan loan providers that offer house purchase and re-finance loans. Home loan rates shown here are based on sample debtor profiles that differ by loan type. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed